Introduction

Are you intrigued by the fast-paced world of trading zero-day options but wary of their complexities? Excellent. In this article, we'll delve into the concept of '0DTE theta decay'—the time decay in zero-days-to-expiration options. Imagine your investment like an ice cube on a hot day; as time ticks away, so does its value. We'll explore how this time decay can both challenge and reward traders in exciting ways. Understanding 0DTE theta decay is crucial for anyone dealing with these rapidly expiring options. Let's dive in and uncover the nuances of this phenomenon, providing you with the insights needed to navigate this high-stakes trading terrain.

What is theta decay in zero day options?

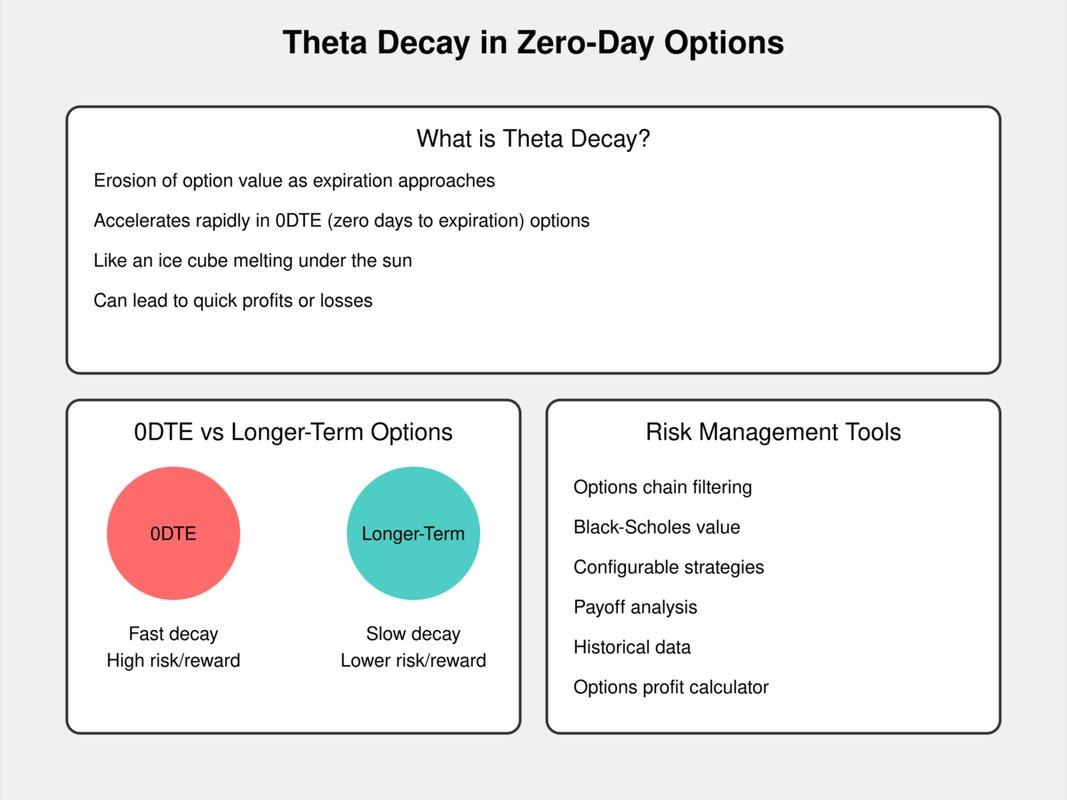

Theta decay in zero-day options is a phenomenon every trader should comprehend. Imagine an ice cube melting under the sun; as time ticks by, its value diminishes. Similarly, theta decay refers to the erosion of an option's value as it approaches expiration. Zero-day options, expiring the same day they're traded, undergo this time decay at an accelerated rate. When you hold such an option, especially if it's out-of-the-money, each passing hour can significantly erode its premium. This time-sensitive nature can be both thrilling and perilous, offering opportunities for keen traders to capitalize on rapid value shifts.Understanding theta decay's impact on zero-day options requires a closer look at how options are priced. The time component, 'theta', is a crucial piece of the pricing puzzle alongside intrinsic value and volatility. As the clock winds down, theta exerts a more potent influence, often outstripping other factors. It's like watching sand slip through an hourglass—inevitable and relentless. For example, if an option has a theta of -0.05, it loses $0.05 in value every hour. On the day of expiration, this effect intensifies, turning the final hours into a race against time for traders seeking profit. So, if you're dabbling in zero-day options, keep a vigilant eye on the clock; it's both your ally and adversary in this high-stakes game.

How fast does theta decay on 0DTE?

Theta decay on 0DTE (zero days to expiration) options is nothing short of a rollercoaster ride. Picture theta as the slow burn of a candle wick: in most cases, it's burning steadily, allowing you to predict its eventual end. But on 0DTE, that wick is suddenly fed a gust of wind, causing it to fizzle out in moments. In the morning, theta might still have a gentle slope; but as the hours pass, especially after noon, the decay accelerates dramatically. By the time the market is nearing close, often the difference between 20 minutes can mean a substantial loss or gain, hinging upon the tiniest segment of time left.Consider an at-the-money option on a volatile stock. At the beginning of the trading day, its premium might still hold significant value due to residual time and volatility. However, as the day progresses, the realistic chance for the stock to make a meaningful move diminishes with each passing second, causing the option's value to collapse swiftly—sometimes within the last 15 minutes. Think of it like an ice cube in the midday desert; it melts slow at dawn but fast under the noon sun. Hence, traders must be agile; a misstep in timing could cost them dearly or make them a fortune in a blink. This hyper-accelerated decay underscores the unique risk and reward profile of 0DTE options, making them a tactical playground for the bold and the swift.

0DTE Theta Decay Curve: Hour-by-Hour Breakdown

Understanding the 0DTE theta decay curve on an hour-by-hour basis gives traders a tactical edge. Theta does not erode option value in a straight line—it follows a convex curve that accelerates as expiration approaches. Here's what a typical trading day looks like for an at-the-money SPX option expiring that same day:

9:30 AM ET (Market Open): The option still carries roughly 6.5 hours of time value. Theta is meaningful but manageable. An ATM SPX option with ~$5.00 of extrinsic value might lose about $0.40–$0.60 in the first hour. Implied volatility from overnight news can temporarily inflate premiums, masking the underlying decay.

10:30 AM – 12:00 PM ET (Mid-Morning): Decay picks up modestly. The option sheds approximately $0.50–$0.80 per hour. Many traders use this window to enter short premium positions because decay is steady but the option still has enough value to collect meaningful credit.

12:00 PM – 1:00 PM ET (Midday): The inflection point. This is where the theta decay curve begins to steepen noticeably. An ATM option that started the day at $5.00 might now be worth $2.00–$2.50, having lost nearly half its value in just 2.5 hours. Traders who are long options and haven't seen the expected move often cut positions here to salvage remaining premium.

1:00 PM – 2:30 PM ET (Afternoon Acceleration): Theta becomes aggressive. The option might lose $0.80–$1.20 per hour. Gamma also spikes during this period, meaning small moves in the underlying can cause outsized swings in option price. This creates a tug-of-war between theta draining value and gamma amplifying directional moves.

2:30 PM – 3:30 PM ET (Final Hour Approach): Decay is now relentless. An ATM option that was worth $5.00 at open might be down to $0.50–$1.00. The rate of decay per minute is several times what it was in the morning. Market makers widen spreads, and liquidity can thin out.

3:30 PM – 4:00 PM ET (Last 30 Minutes): This is where 0DTE theta decay reaches its most extreme. Options that are even slightly out of the money can go from $0.50 to $0.05 in minutes. Only intrinsic value survives. Extrinsic value is essentially vaporized. Traders still holding short premium positions watch their profits lock in rapidly, while long option holders face near-certain loss unless the option is deep in the money.

The key takeaway from this hour-by-hour breakdown: roughly 60–70% of an ATM 0DTE option's time value erodes in the final three hours of trading. Traders who understand this curve can time entries and exits far more effectively.

What is the risk of 0DTE options?

The risk of 0DTE (zero days to expiration) options lies in their extreme volatility and the rapid decline in time value, which can lead to substantial financial losses in a very short period. These options, expiring on the same day they are traded, offer a high reward potential but at the cost of magnified risk. Essentially, trading 0DTE options is like playing with dynamite; the smallest market move can result in significant profits or catastrophic losses due to their high sensitivity to underlying asset price changes. This risk is compounded by the fact that there's virtually no time for the trader to recover from an adverse price movement.Consider a scenario where a trader purchases a 0DTE call option on a stock anticipating a price surge from positive earnings reports. If the stock price doesn't move as expected—perhaps it even drops contrary to the trader's anticipation—the option could rapidly lose all its value, leaving the trader with a total loss. Additionally, the lack of time to manage or adjust their position increases the pressure on traders to predict short-term market movements accurately, which is notoriously difficult even for seasoned investors. Managing these options demands rigorous discipline and risk management strategies, otherwise, the financial repercussions can be swift and devastating.

Comparison of theta decay in 0DTE options vs. longer-term options

Theta decay, or the erosion of an option's value over time, behaves markedly differently in 0DTE (zero days to expiration) options compared to those with longer terms. In the realm of 0DTE options, theta decay accelerates aggressively. Imagine watching ice cubes melt in the sun; as the expiration date approaches, the value of these options evaporates at a breathtaking pace. For traders, this represents both a potential windfall and a significant risk. On one hand, the rapid decay can lead to lucrative gains from premium collection strategies if the market behaves as expected. On the other hand, the compressed timeline leaves little room for error, making these options akin to ticking time bombs.In contrast, longer-term options exhibit a more gradual theta decay. Think of a slow-burning candle; while the passage of time still erodes value, it does so more predictably and less dramatically. This slower rate allows traders to develop and execute more complex strategies involving time spreads or straddles, providing a cushion against sudden market moves. For investors eyeing longer-term options, the extended timeline offers the chance to benefit from strategic adjustments and earns positional advantages over an extended horizon.

Theta Decay Comparison: 0DTE vs 7DTE vs 30DTE vs 90DTE

To put the differences into concrete numbers, consider the following comparison for an at-the-money SPX option with approximately $5,000 underlying value. These figures represent typical daily theta values expressed as a percentage of the option's total premium:

0DTE (Same-Day Expiration)

- Daily theta as % of premium: 100% (all extrinsic value gone by close)

- Hourly decay rate (final 3 hours): ~20–25% of remaining premium per hour

- Decay pattern: Exponential, with most decay in afternoon hours

- Best for: Premium sellers seeking rapid income, scalpers

7DTE (One Week to Expiration)

- Daily theta as % of premium: ~12–18%

- Hourly decay rate: ~0.5–0.8% of remaining premium per hour

- Decay pattern: Accelerating but still manageable intraday

- Best for: Weekly iron condors, short strangles, credit spreads

30DTE (One Month to Expiration)

- Daily theta as % of premium: ~3–5%

- Hourly decay rate: ~0.1–0.2% of remaining premium per hour

- Decay pattern: Nearly linear on a daily basis

- Best for: Monthly income strategies, covered calls, calendar spreads

90DTE (Three Months to Expiration)

- Daily theta as % of premium: ~1–2%

- Hourly decay rate: Negligible intraday

- Decay pattern: Very gradual, almost flat day-to-day

- Best for: LEAPS, long-term directional bets, diagonal spreads

The relationship between time to expiration and theta decay follows the inverse square root of time. This means theta for a 0DTE option can be 5–10x greater than a 30DTE option of the same strike and underlying. For premium sellers, this makes 0DTE incredibly efficient for collecting income—but it also means buyers face an uphill battle against the clock from the moment they enter the trade.

How to Trade Around Theta Decay on Expiration Day

0DTE theta decay creates distinct opportunities depending on whether you are selling or buying premium. Here are proven approaches that experienced traders use to work with—not against—the clock:

Selling Premium Into the Decay

The most popular 0DTE strategy is selling options to collect premium and letting theta do the work. Common setups include:

-

0DTE Iron Condors: Sell an out-of-the-money call spread and put spread simultaneously. As long as the underlying stays between your short strikes, theta decay works entirely in your favor. Many SPX traders open iron condors at 9:30–10:00 AM and close them by 2:00–3:00 PM once 50–70% of the credit has been captured.

-

0DTE Credit Spreads: Sell a directional credit spread (bull put or bear call) when you have a market bias. The key is selecting strikes far enough from the current price that theta decay collapses the spread value before the underlying can reach your short strike.

-

Naked Short Options (Advanced): Some traders with significant capital sell naked puts or calls, relying on theta to erode premium. This carries unlimited risk and requires strict stop-losses and position sizing.

Buying Premium With Theta Awareness

If you're buying 0DTE options for a directional bet, theta is your enemy. To mitigate its impact:

-

Trade early in the session. You have maximum time value and the decay rate is slower in the morning. A directional move in the first 90 minutes gives you the best chance of profiting before theta accelerates.

-

Use tight stops. If the trade doesn't work within 30–60 minutes, exit. Holding a losing long option position on expiration day is the fastest way to watch capital evaporate.

-

Size down. Because the all-or-nothing nature of 0DTE amplifies outcomes, position sizing should be smaller than for longer-dated trades—typically 1–2% of account value per trade.

The Gamma-Theta Tradeoff

On expiration day, gamma and theta are at war. Gamma measures how quickly delta changes, and on 0DTE it reaches extreme levels for ATM options. This means a sudden $5 move in SPX can turn a $0.50 option into $5.00—or a $5.00 option into $0.50. Skilled traders use this dynamic by:

- Selling options when they expect low volatility (theta wins)

- Buying options just before expected catalysts like Fed announcements or economic data releases (gamma wins)

Understanding this tradeoff is the single most important skill for consistent 0DTE profitability.

Underlying factors influencing theta decay in 0DTE options

Theta decay, especially in 0DTE (zero days to expiration) options, is predominantly influenced by time decay's relentless march towards the expiration bell. When holding a 0DTE option, the race against the clock becomes palpable; each passing minute erodes the premium's time value. Picture options as melting ice cubes on a hot sunny day. As the day progresses, those ice cubes—representing the time value—become smaller and smaller. The closer an option gets to its expiration, the faster its time value diminishes—a phenomenon known as accelerated time decay.Another critical factor at play is volatility. On a 0DTE option, the market's perception of the underlying asset's potential volatility becomes intensely focused. Higher implied volatility can temporarily inflate premiums, but as the trading day wanes and actual movement is observed, volatility often drops, compounding theta decay. Have you ever come across a brewing storm that ultimately dissipates, leaving barely a drizzle? This scenario mirrors the decreasing implied volatility as the unpredictable potential diminishes into reality, resulting in sharp declines in option value. Additionally, proximity to the strike price intensifies theta decay. OTM (out-of-the-money) options face a steep uphill battle to expire ITM (in-the-money), making theta's bite much more aggressive. In contrast, ITM options see their intrinsic value safe but are not immune to the ravages of theta on their time value. Understanding these underlying forces helps traders navigate the ephemeral world of 0DTE options with sharper insight.

Tracking 0DTE Theta in Excel with MarketXLS

One of the most practical ways to monitor 0DTE theta decay in real time is by using MarketXLS in Excel. Instead of relying on your broker's options chain—which may update slowly or lack customization—you can build a live theta tracking dashboard that refreshes automatically.

Pulling the Live Option Chain

Use the =QM_GetOptionChain("^SPX") function to retrieve the complete SPX option chain directly into Excel. This returns all available strikes, expirations, bid/ask prices, and volume data. To focus on 0DTE contracts, filter for today's expiration date. The data refreshes in real time, giving you a live view of how premiums are changing throughout the day.

Monitoring Greeks in Real Time

The =QM_GetOptionQuotesAndGreeks("^SPX") function is where the real power lies for theta tracking. This function returns the full Greek suite—delta, gamma, theta, vega, and rho—for every option in the chain. You can:

- Sort by theta to identify which strikes are decaying fastest

- Compare theta values between ATM, OTM, and ITM options

- Track how theta changes hour by hour as expiration approaches

- Spot anomalies where theta is unusually high or low relative to implied volatility

Building a Theta Decay Dashboard

Here's a practical setup for monitoring 0DTE theta decay:

- Cell A1:

=Last("SPY")— displays the current SPY price as a quick reference for the underlying market level - Row 3 onward:

=QM_GetOptionChain("^SPX")— pulls the full option chain - Adjacent columns:

=QM_GetOptionQuotesAndGreeks("^SPX")— overlays Greeks onto the chain - Conditional formatting: Apply color scales to the theta column so that rapidly decaying options turn red, making it visually obvious which contracts are losing value fastest

- Charting: Create a line chart that plots theta values for your chosen strikes at different times throughout the day. Take snapshots every 30–60 minutes to build the decay curve visually.

This setup allows you to see exactly how 0DTE theta decay behaves across different strikes and throughout the trading session—something no static options chain can provide. Having this data in Excel also lets you build custom alerts, calculate position-level theta exposure, and run scenario analysis on your trades.

Risk Management Tools for 0DTE Trading

To effectively manage risk when engaging in zero days to expiry (0DTE) trading, MarketXLS offers several powerful tools and strategies. Below are some essential risk management tools and functionalities provided by MarketXLS for 0DTE trading:

1) Options Chain Filtering

MarketXLS allows you to filter option chains by various criteria such as expiration dates, strike ranges, and moneynesses (e.g., options with strike prices that are within a specific percentage of the underlying price). This is essential for identifying suitable options to trade 0DTE.

2) Black-Scholes Value

The Black-Scholes model is used in MarketXLS to calculate the fair value of European call-and-put options. It considers the underlying stock's value, strike price, time to expiration, volatility, and interest rate risk. This helps in identifying undervalued or overvalued options, thereby enabling more informed trading decisions.

3) Configurable Option Strategies

MarketXLS enables traders to utilize up to 8 legs in their options trading models. This flexibility allows for complex 0DTE strategies that can be analyzed for risk and reward. For instance:

– Real-time options tracking with Greeks

– Adding underlying buy/sells to view covered call trade results

– Taking snapshots of trade configurations over time in CSV files.

4) Payoff and Results Analysis

Once an options strategy is configured, MarketXLS provides tools to compare the payoff across different legs, adjust volatility, and model different market scenarios. This functionality helps in estimating the potential payouts of an options strategy and saving the results for future reference and backtesting.

5) Saving and Accessing Scans

Traders can save their trade configurations and scanning criteria in MarketXLS. These scans can be saved privately, publicly, or for a team, allowing easy access and continuous improvement based on historical performance.

6) Options Profit Calculator

The Options Profit Calculator in MarketXLS helps estimate potential profits or losses for any options trade. By considering various factors like underlying stock price, strike price, and option expiration date, it ensures a comprehensive analysis of risk and reward.

7) Historical Option Data

MarketXLS provides functionalities to retrieve and analyze historical option data. Functions like opt_HistoricalOptionChain allow users to backtest their strategies by retrieving complete option chains from past dates. This can be particularly useful in understanding how different scenarios might impact 0DTE trades.

Additional Tools

– **Unusual Option Open Interest (OI) Scan **: Identifies significant deviations in open interest, alerting to potential market sentiment shifts.

– High Volume Underlying Scan: Highlights underlying assets with substantial trading volumes, providing clues to market activity.

– ** Put/Call Ratios and Other Greeks**: Offering insights into market sentiment and volatility, aiding better risk assessment.

By leveraging these tools and functionalities in MarketXLS, traders can effectively manage the risks associated with 0DTE trading and make more informed trading decisions. For detailed guidance on using these tools, you may refer to the tutorials and templates available within MarketXLS.

Here is the template you might want to checkout, and MarketXLS has 100s of templates to get you started easily and save you time:

• Template for Accessing Real-Time Data on US Stock Option Bids, Greeks, Open Interest, and Unusual Options Activity**

Link to the template: MarketXLS Template for Accessing Real-Time Data

Image URL of the template:

Template Image

Frequently Asked Questions About 0DTE Theta Decay

What time of day does 0DTE theta decay accelerate the most?

0DTE theta decay accelerates most aggressively in the final 2–3 hours of the trading session (1:00 PM – 4:00 PM ET). During this window, at-the-money options can lose 60–70% of their remaining extrinsic value. The last 30 minutes are particularly brutal—options that are even slightly out of the money can collapse from $0.50 to near zero. Morning sessions (9:30–11:00 AM) see a steadier, more gradual decay rate that gives traders more time to react to market moves.

Can you profit from 0DTE theta decay without selling naked options?

Absolutely. Defined-risk strategies like iron condors, credit spreads (bull put spreads and bear call spreads), and butterfly spreads all allow you to profit from 0DTE theta decay while capping your maximum loss. For example, a 0DTE iron condor on SPX might collect $2.00 in credit with a maximum risk of $3.00—a defined and manageable risk profile. These strategies are popular among traders who want theta decay working in their favor without the unlimited risk exposure of naked positions.

How does implied volatility interact with 0DTE theta decay?

Implied volatility (IV) and theta are deeply intertwined on expiration day. Higher IV inflates option premiums, which means there's more extrinsic value for theta to erode. On days with elevated IV—such as Federal Reserve announcement days or major economic data releases—0DTE options carry larger premiums, and the theta decay in dollar terms is more dramatic. However, IV itself also tends to collapse as the event passes (a phenomenon called "IV crush"), which compounds the effect of theta. Traders selling premium on high-IV expiration days benefit from both theta decay and volatility contraction simultaneously.

What is the difference between theta decay and gamma risk on 0DTE?

Theta and gamma are opposing forces on expiration day. Theta steadily erodes option value with the passage of time, benefiting sellers. Gamma, on the other hand, measures how quickly an option's delta changes as the underlying moves—and on 0DTE, gamma reaches extreme levels for at-the-money options. This means a sudden price move can cause an option's value to spike dramatically, temporarily overwhelming theta's erosion. Premium sellers want calm, range-bound markets where theta dominates. Premium buyers need swift, large moves where gamma overpowers theta. The balance between these two Greeks defines the risk-reward profile of every 0DTE trade.

Is 0DTE theta decay the same for SPX and individual stock options?

Not exactly. SPX options are European-style (cash-settled, no early exercise risk) and have the most liquid 0DTE market. Individual stock options are American-style, which introduces early assignment risk—particularly for in-the-money short options near expiration. Additionally, individual stocks can experience idiosyncratic moves (earnings surprises, analyst upgrades) that overwhelm theta decay, while SPX tends to be smoother due to index diversification. Most professional 0DTE theta decay strategies focus on SPX or SPY for this reason.

How can I track 0DTE theta decay in real time?

The most effective way to track 0DTE theta decay in real time is by using MarketXLS in Excel. The =QM_GetOptionQuotesAndGreeks("^SPX") function returns live Greek values—including theta—for every strike in the SPX option chain. You can build a dashboard that refreshes automatically, apply conditional formatting to highlight the fastest-decaying strikes, and chart the theta curve throughout the trading day. This gives you a significant advantage over traders relying on static broker platforms. Get started with MarketXLS to build your own real-time theta tracking workbook.

Summary

The article discusses the fast-paced trading of zero-day options and demystifies theta decay. Theta decay erodes an option's value as it nears expiration, accelerating rapidly in 0DTE options. This fast decay can lead to quick losses or gains, like an ice cube melting under the sun. Understanding this time decay is crucial for zero-day options trading.

Theta decay in 0DTE options intensifies, especially afternoon hours, making timing crucial. Risks include extreme volatility and rapid loss in value, likened to playing with dynamite. Comparing 0DTE to long-term options, 0DTE has faster decay, like ice cubes melting under the sun, versus a slow-burning candle for longer-term options.

Risk management tools are vital, and MarketXLS offers functionalities like options chain filtering, the Black-Scholes value for fair pricing, configurable strategies, payoff analysis, and historical data. These tools help traders make informed decisions and manage the heightened risks in 0DTE trading. Ready to track 0DTE theta decay in real time? Try MarketXLS today and build your own expiration-day trading dashboard.

0dte theta decay

0dte theta decay