– A Wait and Watch Story Right Now")

Tesla, Inc. (TSLA), one of the global market leaders in the electric vehicle industry, recently made headlines on Wall Street because of a crash of 65%+ in the stock price.

The crash may be attributed to rising competition in the EV market, performance not meeting expectations, Musk’s Twitter distraction, restrictions placed in China (one of Tesla’s manufacturing hubs), and Musk selling massive amounts of Tesla shares.

In this article, we will comprehensively analyze the current position of Tesla (TSLA) by using three different valuation techniques to determine a fair value estimate of the company and by evaluating how Tesla is tackling the plethora of obstacles it faces.

Tesla is a multinational automotive and clean energy company headquartered in Austin, Texas, US. The company primarily manufactures and sells various models of electric vehicles with innovative features, including autopilots. A small segment of the company’s business also comes from energy storage and generation products. Most of the company’s revenue comes from the USA and China, with the company now expanding to more than 30 other countries.

Latest Happenings in Tesla (TSLA):

Tesla’s China plant had to suspend production of Model Y in the last week of December due to COVID-19 restrictions, which led to a cut in planned production for this model of about 30%.

Tesla’s delivery numbers fell shy of the company’s target primarily because of the lowering demand and increasing competition. In addition, the subsidies ending for electric vehicles in China add fuel to this problem and will increase costs which can further decrease the already sluggish demand. So, to sustain the volume of deliveries and regenerate the demand, Tesla has cut prices of top models by 6-13.5%.

Tesla is also planning to start early production of the highly anticipated cyber truck in the Austin plant by mid-2023 and will start mass production by the end of 2023. The cyber truck is a unique-looking vehicle that provides solid performance with superior durability and strength.

In addition, the product consists of features like the Tesla armor glass, hexagonal wheel arches, and the ability to go from 0 to 60 mph in 2.9 seconds. All these lucrative features separate Tesla from the competition, which is why the vehicle already has one million+ reservations.

The CEO, however, announced that the price of the Cybertruck would increase from the initially mentioned price as inflation and supply chain issues have increased the cost of production, which might lead to a fall in the reservations and may decrease the possible profit margins of the product. However, if the product lives up to the hype and demand scales up fast, it has the potential to crack the highly profitable truck market and become a significant source of revenue for Tesla.

Financials (TSLA)

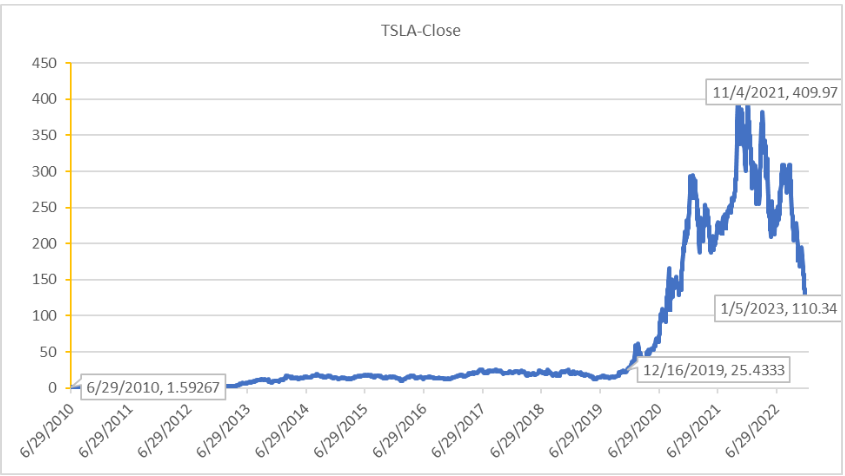

It has been quite a journey for TSLA holders, from $1.50 in 2010 to $25 right before the pandemic, then touching an ATH of $410, then dropping to the $110 range, and then again rising by 75%+ in the last one month(all prices adjusted for splits). In its journey of over a decade, TSLA has undergone two major stock splits, a 5-for-1 in 2020 and a 3-for-1 in 2022. In other words, an investment of $1,000 during its IPO would fetch roughly 59 stocks, which today would have been approximately 885 shares worth $361,965 (a 36,000% return) at its ATH and $97,350 ( 9,635% return) at the start of Jan 2023.

From 2010 to 2021, the company’s revenue has grown by an absolute 46,003% (CAGR 75%), effectively doubling the company’s revenue every year. Considering the past five years, the revenue CAGR stands at approximately 50%, which is also phenomenal.

However, the profits started in 2020 with an NPM of 2.3%, closing at 10.25% in 2021. From 2020 to 2021, the profits grew by a mind-boggling 665% from $721M in 2020 to $5.5B in 2021. We expect 2022 numbers to be even better as TSLA reported a 40% YoY growth in vehicle deliveries.

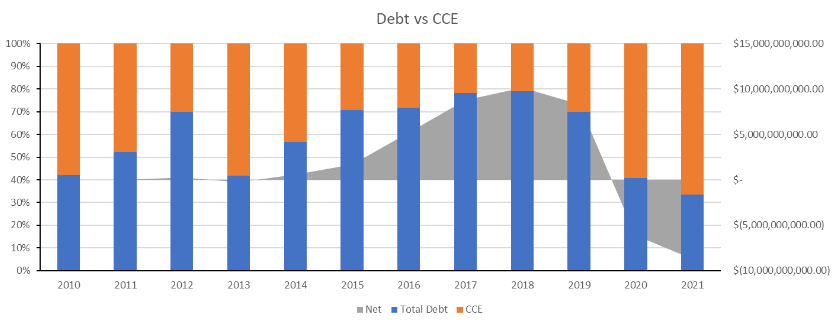

TSLA has also made smart decisions to maintain its financial health and reduce the net debt on its balance sheets. At the end of 2021, the net debt stood at -$8B compared to +$10B in 2018.

The company has an F-Score of 8 out of 9, indicating that the financials are strong. Financial investors use this score to find the best-value stocks (nine being the best). It is calculated based on key financial metrics like return on assets, operating cash flow, current ratio, asset turnover ratio, and gross margin.

Valuations (TSLA)

Tesla (TSLA), a global leader in electric vehicle manufacturing, has seen a tough year in the stock market. Over the last 12 months, the stock has dropped by 65% and has continued to underperform till 1st week of Jan 2023, despite the company reporting solid revenues and net profit growth for the current quarter. However, in the last month, It declared its last quarter result, beat all the expectations, and rose 75%+ in just one month.

There is currently a lot of news regarding CEO Elon Musk and his recent acquisition of Twitter. Another macroeconomic factor that contributed to Tesla’s underperformance is the continuous rate hikes by the Federal Reserve, which have led to a deteriorating market environment. Additionally, the shares are currently under pressure from the short position by Bill Gates and ‘The Big Short’ legend Michael Burry.

However, we believe that Tesla’s long-term growth prospects remain strong and that the company is well-positioned to weather the current market challenges. However, the share price trades with a hefty premium over other players in the industry and can languish in time to come. Therefore, let’s perform different valuation techniques to estimate Tesla’s fair value.

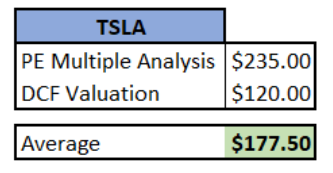

P/E Multiple Valuation

We looked at the Tesla financials since it was listed on the exchange in 2010 and found some interesting facts about it.

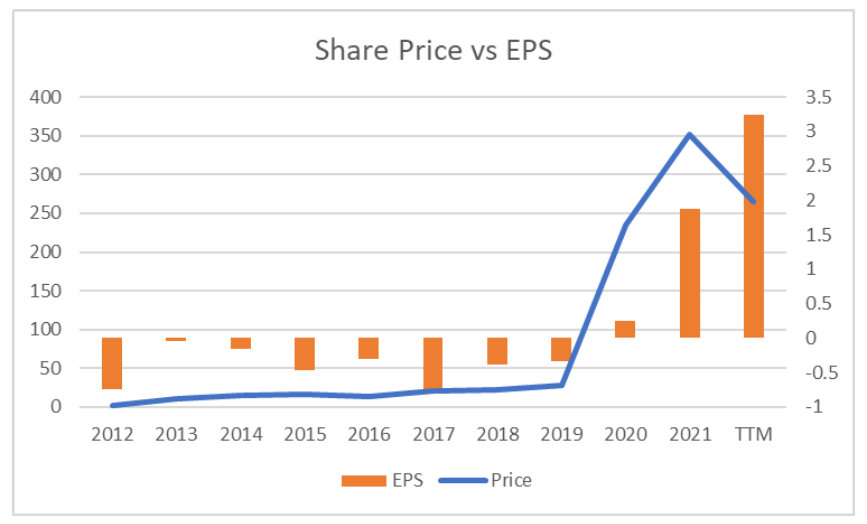

Tesla has been a loss-making company for the last decade, and finally, since the second quarter of the Financial Year 2020, it started reporting profits. Once Tesla became a profitable company, its profits grew enormously. Analyze it chronologically:

- FY 2019 annual EPS was $-0.33, a 14% decline from 2018.

- FY 2020 annual EPS was $0.25, which finally turned positive after nine years.

- FY 2021 annual EPS was $1.87, a 648% increase from 2020.

- EPS for the twelve months ending December 31, 2022, was $4.02, a 115% increase year-over-year.

- EPS for the quarter ending December 31, 2022, was $1.18, a 55% increase year-over-year.

From this, being the leader in the EV industry and showcasing continuous improvement, Tesla is poised to grow in an almost similar fashion for some more time before the competitors start showing improvements.

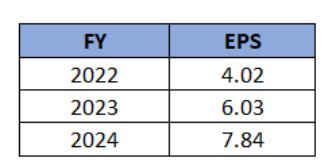

Taking cues from history, we expect the company to continue to grow, but the extraordinary growth will plateau in the next 3 to 5 years. As a result, we expect the company to report 50% YoY growth in FY 2023 and 30% in FY 2024.

Tesla has always commanded a median PE ratio of 18, but it exploded in the last two years to 1,100, and now it stands at 53. We expect that Tesla will continue its journey towards mean reversion, and at the end of two years, it will reach a PE of 30. Per the assumptions, Tesla’s share price may reach $235 in the next two years.

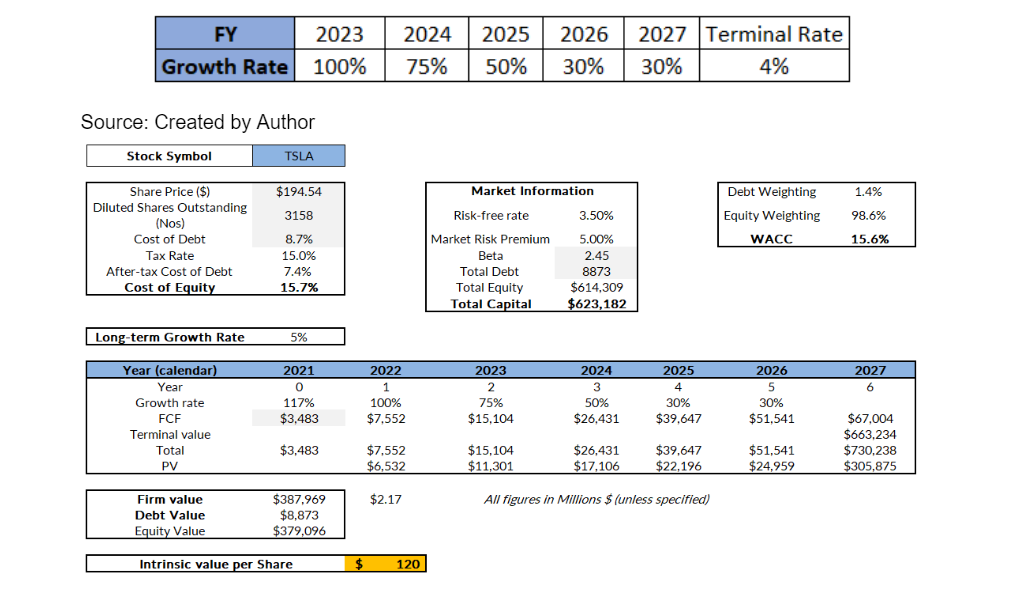

DCF Valuation:

A couple of assumptions have been made by us to perform this DCF valuation.

- Risk-Free Rate: Looking at the current market, we have assumed it as 3.5%.

- Market Risk Premium: According to our assumptions, it would be about 5%.

- Free Cash Flow Growth Rate: We have assumed growth based on industry and company outlook.

Based on the assumptions stated above, we undertook a DCF analysis, and with such an expected growth figure in free cash flow, the intrinsic share value comes out to be $120.

Peer Valuation:

We looked at the various companies listed in the US, like Mercedes-Benz Group AG (MBGAF), General Motors Company (GM), and Ford Motor Company (F), to compare Tesla. Still, all these are legacy automobile companies and not in the pure Electric Vehicle segment. Hence, we can’t do the peer valuation for TSLA.

After two valuation model calculations, the average fair value of Tesla turns out to be $177.50.

While Tesla (TSLA) has enjoyed the dream run in the last two years, followed by a sharp correction, it has finally approached its fair value. However, last month’s sharp move has made it a little expensive again. Any sharp correction again can make it a value-buy.

Risks

The company has faced a lot of hurdles in recent times, which have impacted the company’s performance and its stock price. One risk is the increasing competition in the EV industry. Various automobile giants such as Ford, General Motors, Nissan, and BMW have realized the importance electric vehicles hold in the future and have entered this industry.

As a result, Tesla’s market share has dropped from 80% in 2020 to 65% in 2022. With more competitors coming in, Tesla’s dominance in the EV sector is starting to fade away. Companies like BYD Auto selling more cars than Tesla in the APAC market is a testament to the company’s fading dominance. In addition, India is considered one of the fastest-growing countries in the world, which Tesla tried to enter but had to backtrack when BYD Auto started selling its EV in India.

Another risk faced by the company is the CEO Elon Musk’s Twitter distraction. Musk has sold over 40 billion worth of stock in the last two years to fund his Twitter purchase. As a result, investors and stakeholders are concerned as Musk would give lesser time to Tesla as his focus is split after the Twitter purchase.

With the threat of COVID-19 still looming over China, which accounts for 23% of Tesla’s revenue, consumers are controlling their spending, which can significantly reduce the demand and result in a drop in Tesla’s revenue from China. In addition, the stringent COVID-19 policies of the country may lead to supply chain issues, especially with semiconductors which might affect Tesla’s production in other countries.

Furthermore, Tesla is diversifying into the pickup truck market by launching the cybertruck in 2023. Although the cybertruck is highly awaited by many, Elon Musk recently announced that the cost of production would increase, which will increase the price of the cybertruck. With an increase in the price, the demand would inevitably decrease, which is not an excellent sign for a new product. Furthermore, rising interest rates and the fear of recession may further plummet the demand.

Conclusion

Despite all the company’s risks, Tesla (TSLA) is still the most established and prominent brand in the EV industry. As it has been in the market for longer and solely focuses on EVs, it has a competitive advantage over other companies. We have determined Tesla’s fair value as $177.5, which is lower than its current stock price. Hence we believe it is over-valued. If the stock’s price falls due to external factors, it can be a great value buy for the future.