Beneish M-Score- A Tool To Find The Manipulation Of The Earnings.

Meet The Ultimate Excel Solution for Investors

- Live Streaming Prices Prices in your Excel

- All historical (intraday) data in your Excel

- Real time option greeks and analytics in your Excel

- Leading data in Excel service for Investment Managers, RIAs, Asset Managers, Financial Analysts, and Individual Investors.

- Easy to use with formulas and pre-made sheets

The extent to which earnings are manipulated has long been a question of interest to analysts, regulators, researchers, and other investment professionals. To address this issue, Professor Messod Beneish developed the Beneish M-score model and published it in a paper in June 1999 called The Detection of Earnings Manipulation.

Beneish M score is a Mathematical model designed to find out the manipulation in the company’s earnings. Beneish’s M-Score model uses eight variables weighted by coefficients to identify whether a company has manipulated its profits.

How is it calculated?

1.Days’ Sales in Receivables Index (DSRI)-

DSRI is the ratio of days sales in receivables in a year to the previous year. If the value of DSRI > 1, it is an indicator of revenue inflation. An increase in the value of DSRI indicates that the company has followed the lenient credit policy or allowed the higher credit period to increase the sales.

DSRI = (Net Receivablest / Salest) / (Net Receivablest-1 / Salest-1)

2. Gross Margin Index(GMI)-

GMI is the ratio of gross margin of a year to the previous year. When GMI is greater than 1, it indicates that gross margins have deteriorated. A firm with a declining gross profit margin is more likely to manipulate earnings.

GMI = [(Salest-1 – COGSt-1) / Salest-1] / [(Salest – COGSt) / Salest]

3. Asset Quality Index (AQI)-

Asset quality in a given year is the ratio of non-current assets other than property plant and equipment (PPE) to total assets. If AQI > 1, it indicates that the firm has potentially increased its involvement in cost deferral.

AQI = [1 – (Current Assetst + PP&Et + Securitiest) / Total Assetst] / [1 – ((Current Assets t-1+ PP&E t-1 + Securities t-1) / Total Assets t-1)]

4. Sales Growth Index (SGI)-

SGI is the ratio of sales of a year to the previous year. The value of SGI > 1 indicates that the company’s sales have increased compared to last year.

High sales growth does not imply manipulation, but high growth companies are more likely to commit financial fraud because their financial position and capital need pressure managers to achieve earnings targets.

SGI = Salest / Salest-1

5. Depreciation Index (DEPI)-

DEPI is the ratio of the rate of depreciation in the previous year to the current year. The value of DEPI higher than 1 indicates the company has revised the life of its useful asset to provide a better picture of its profits.

DEPI = (Depreciation t-1/ (PP&E t-1 + Depreciation t-1)) / (Depreciation t / (PP&E t + Depreciation t))

6. Sales, General, and Administrative Expenses (SGAI)-

SGAI measures the ratio of Sales, General, and Administrative expenses to the prior year. The value of SGAI > 1 indicates that SGA expenses as a percentage of sales increased in the current year. An increase in the SGA expenses leads to a reduction in the operating profits. Management may try to cover up this through manipulation.

SGAI = (SG&A Expense t / Sales t) / (SG&A Expense t-1/ Sales t-1)

7. Leverage Index (LVGI)-

LVGI is the ratio of total debt to total assets in a year relative to the corresponding ratio with the previous year. An LVGI greater than 1 indicates an increase in leverage. Increased leverage results in an increase in the interest expenditure, Thus affecting the company’s net profits. Increased leverage increases the chances of manipulation of earnings.

LVGI = [(Current Liabilities t + Total Long Term Debt t) / Total Assets t] / [(Current Liabilities t-1 + Total Long Term Debt t-1) / Total Assets t-1]

8. Total Accruals to Total Assets (TATA)-

Accruals measures the difference between the accounting Profit/(loss) and the cash profit/(loss). Larger discrepancies in the accounting profits and cash profits increase the probability of manipulation of the earnings.

TATA = (Income from the Continuing Operations t – Cash Flows from the Operations t) / Total Assets t

Based on the above eight variable M-score can be calculated as follows:

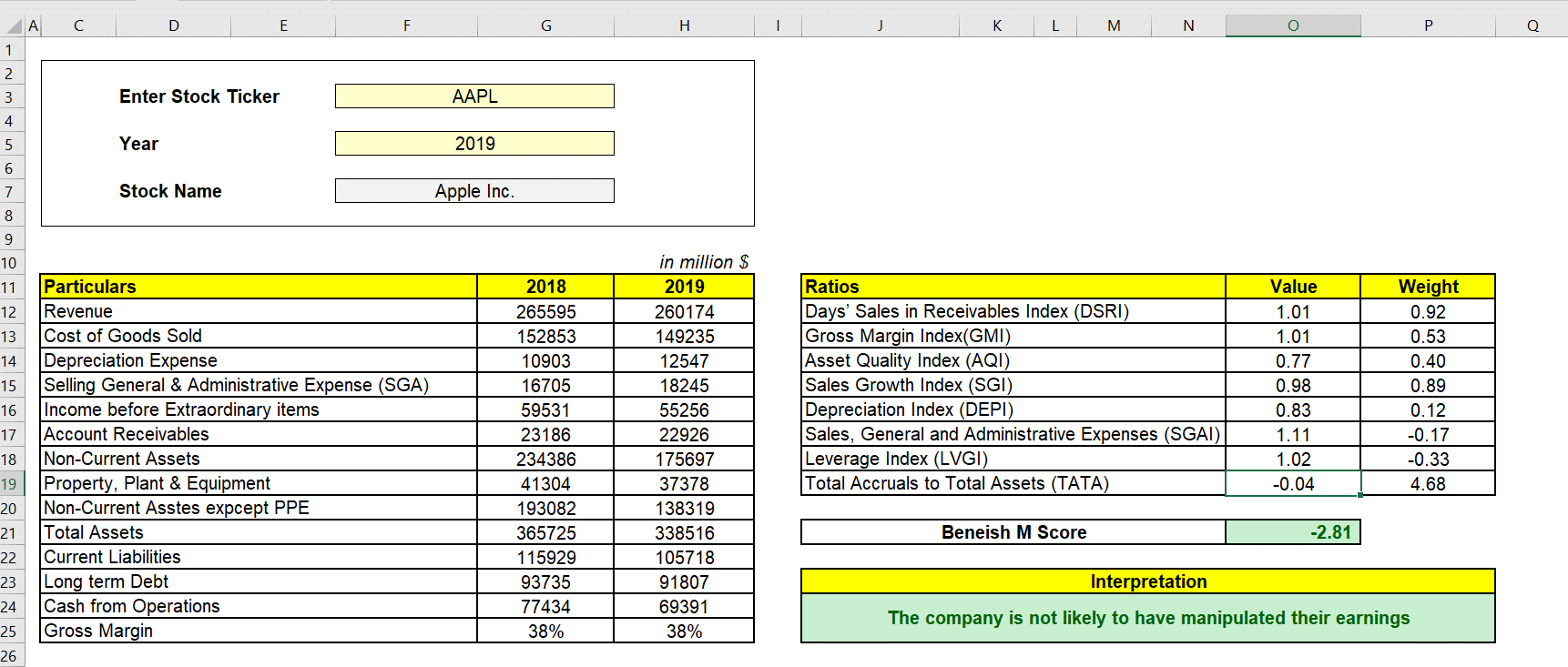

M Score = -4.840 + 0.920 x DSRI + 0.528 x GMI + 0.404 x AQ + 0.892 x SGI + 0.115 x DEPI – 0.172 x SGAI – 0.327 x LVGI + 4.697 x TATA

We can draw two possible conclusions using the M score:

- Beneish M Score < -2.22: the company is not likely to have manipulated its earnings

- Beneish M Score > -2.22: the company is likely to have manipulated its earnings.

Let us find out the M-score of Apple with the MarketXLS template.

Limitations of the model-

- Beneish’s M-score model uses to find the manipulation of the overstated profits. We cannot use it to find the understated profits.

- The Beneish model does not apply to financial firms like banks and insurance companies.

- The Beneish model is a probability theory model and doesn’t guarantee fraud detection in a company.

Successful Application of Beneish Model-

In 1998, a group of Cornell University business students used the Beneish model and correctly identified that the Enron Corporation was manipulating its earnings. At that time, Enron’s stock was trading at $48. Noticeably, Wall Street’s financial analysts didn’t pay heed to this and still recommending a buy for the stock. Eventually, the stock went up to $90. In 2001, when Enron filed for bankruptcy, it was found out that Enron manipulated its earnings, and it results in a $74 billion loss to the shareholders.

I invite you to book a demo with me or my team to save time, enhance your investment research, and streamline your workflows.