Conversion Arbitrage Options Strategy

Meet The Ultimate Excel Solution for Investors

- Live Streaming Prices Prices in your Excel

- All historical (intraday) data in your Excel

- Real time option greeks and analytics in your Excel

- Leading data in Excel service for Investment Managers, RIAs, Asset Managers, Financial Analysts, and Individual Investors.

- Easy to use with formulas and pre-made sheets

Conversion arbitrage is an options trading strategy to take advantage of perceived inefficiencies present in the pricing of options. Also known as reversal-conversion (or reverse conversion), it is a strategy where the trader buys a put and writes a covered call (a call on a stock that they already own) with identical strike prices and expiration dates. It is considered a risk-neutral strategy where the trader profits when the call option is overpriced, or the put is underpriced due to market inefficiencies, or from mis-priced interest rate assumptions.

How to Implement Conversion Arbitrage?

Conversion Arbitrage is best implemented when you believe that the options are overpriced relative to the underlying stock. It is an options arbitrage strategy that takes advantage of discrepancies in the value of synthetic positions, and they’re represented equally to return a risk-free profit. However, the profit that can be earned using this strategy is limited.

In this strategy, traders go long on the underlying stock, and the ATM put option contract, and short on the ATM call option contract. Both the options are of the same underlying security and have the same expiration date.

To implement conversion arbitrage options strategy, they buy the underlying stock and simultaneously offset that trade with an equivalent synthetic short stock position (long put + short call). As a result, the long stock position carries a positive 100 delta, while the synthetic short stock position using options has a negative 100 delta, making the strategy delta neutral or insensitive to the market’s direction.

Example (Using MarketXLS Template)

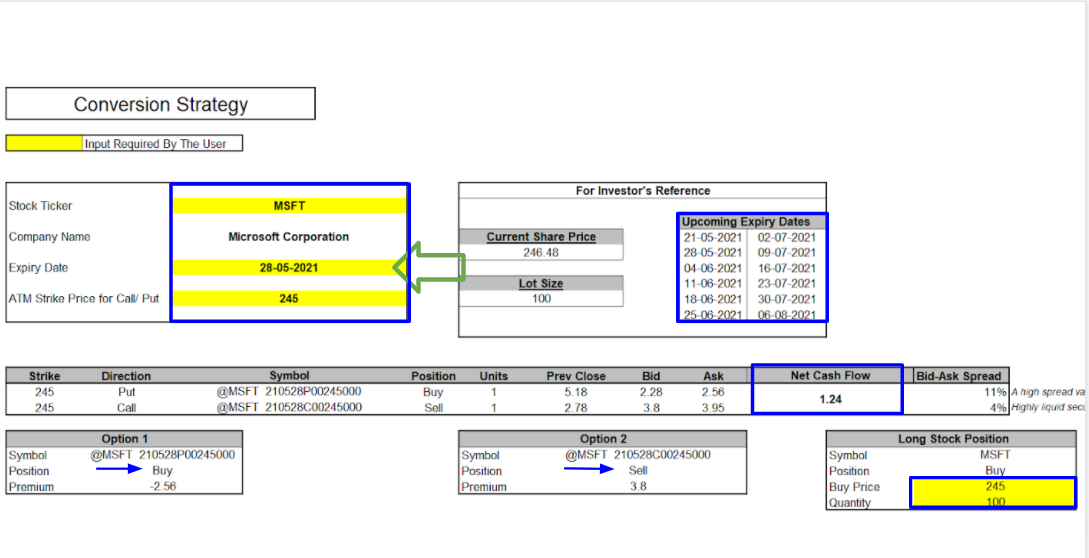

MarketXLS provides a template for this strategy. The yellow cells have to be inputted by the user. Here, Provide the Stock Ticker, Expiry Date, ATM strike price for Call/Put, and the Buy Price and Quantity of the long stock. Upcoming expiry dates are available for reference.

We have used Microsoft (Nasdaq: MSFT), Expiry date as 28 May 2021, ATM strike price is 245 and the Buy Price and Quantity of the long stock is 245 and 100. So voila, we have built the Conversion Arbitrage Strategy for MSFT.

We have entered into a long stock position of MSFT with the buy price and quantity 245 and 100. And on the options front, we have bought 1 ATM $245 put option contract and sold 1 ATM $245 call option of MSFT. As a result, we have built the net credit strategy and received 124 dollars outright to enter into the trade, reflected in the net cash flow section.

Find this template here: https://marketxls.com/template/conversion-reverse-arbitrage-strategy

A payoff schedule and payoff diagram are available in the template too. They can be used to analyze the maximum gain, loss, and break-even.

Maximum gain is limited and is locked in immediately when the conversion arbitrage is done, as shown by the blue box. It can also be computed using a formula:

Profit = Strike Price of Call/Put – Purchase Price of Underlying + Call Premium – Put Premium.

Being a risk-free strategy, it is insensitive to the market’s direction, so there are no chances of a loss. However, the difference between the synthetic position and its actual instrument is usually so small that it hardly justifies the commissions paid on the position.

The Bottom Line

Arbitrage opportunities enable investors to earn risk-free profits, and hence these opportunities are absorbed by the market and fade away very quickly. Additionally, transaction costs such as broker fees and margin interest for executing options and short-selling stock involving apparent arbitrage opportunities may not exist in practicality.

Disclaimer

All trademarks referenced are the property of their respective owners. Other trademarks and trade names may be used in this document to refer to either the entity claiming the marks and names or their products. MarketXLS disclaims any proprietary interest in trademarks and trade names other than its own, or affiliation with the trademark owners.

None of the content published on marketxls.com constitutes a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The author is not offering any professional advice of any kind. The reader should consult a professional financial advisor to determine their suitability for any strategies discussed herein. The article is written for helping users collect the required information from various sources deemed to be an authority in their content. The trademarks if any are the property of their owners and no representations are made.

I invite you to book a demo with me or my team to save time, enhance your investment research, and streamline your workflows.