Option Strategies-Long Straddle(Excel Template)

")

Meet The Ultimate Excel Solution for Investors

- Live Streaming Prices Prices in your Excel

- All historical (intraday) data in your Excel

- Real time option greeks and analytics in your Excel

- Leading data in Excel service for Investment Managers, RIAs, Asset Managers, Financial Analysts, and Individual Investors.

- Easy to use with formulas and pre-made sheets

Long straddle

A long straddle is an options strategy comprised of buying both an ATM call option and an ATM put option with the same strike price and expiration date. It is used when the trader believes the underlying asset will move significantly higher or lower over the options contracts’ lives. The maximum loss is the amount of premium given while buying the options. The maximum profit can be unlimited if the stock moves sharply in either direction. Volatility is the main factor in this strategy. A trader loses if the underlying ends up flat or doesn’t move significantly. Let’s understand this strategy with the marketXLS template.

Using marketXLS

Below is a screenshot of the complete template that marketXLS provides for this strategy. This template has five major components. Let’s break them down one by one.

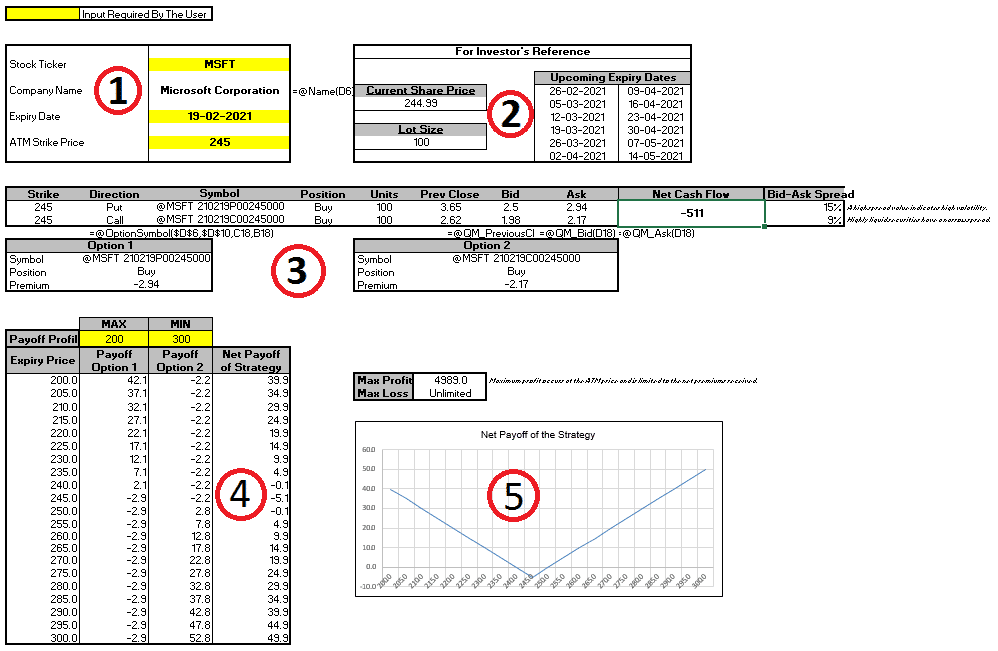

Input by user

In this section, you put the stock ticker and the expiry for the option of that underlying. You can select the expiry from section 2. Here, we have taken the example of MSFT (Microsoft Corporation) with an expiry of 19 Feb 2021.

Execution

A long straddle involves buying two ATM calls and put at the same strike and expiry. That’s exactly what the template shows—two legs of MSFT at $245 with an expiry of 19 Feb 2021. As a result, a net debit spread of $511 is created, which means you pay upfront to open this trade. This is the maximum loss you would incur in this trade.

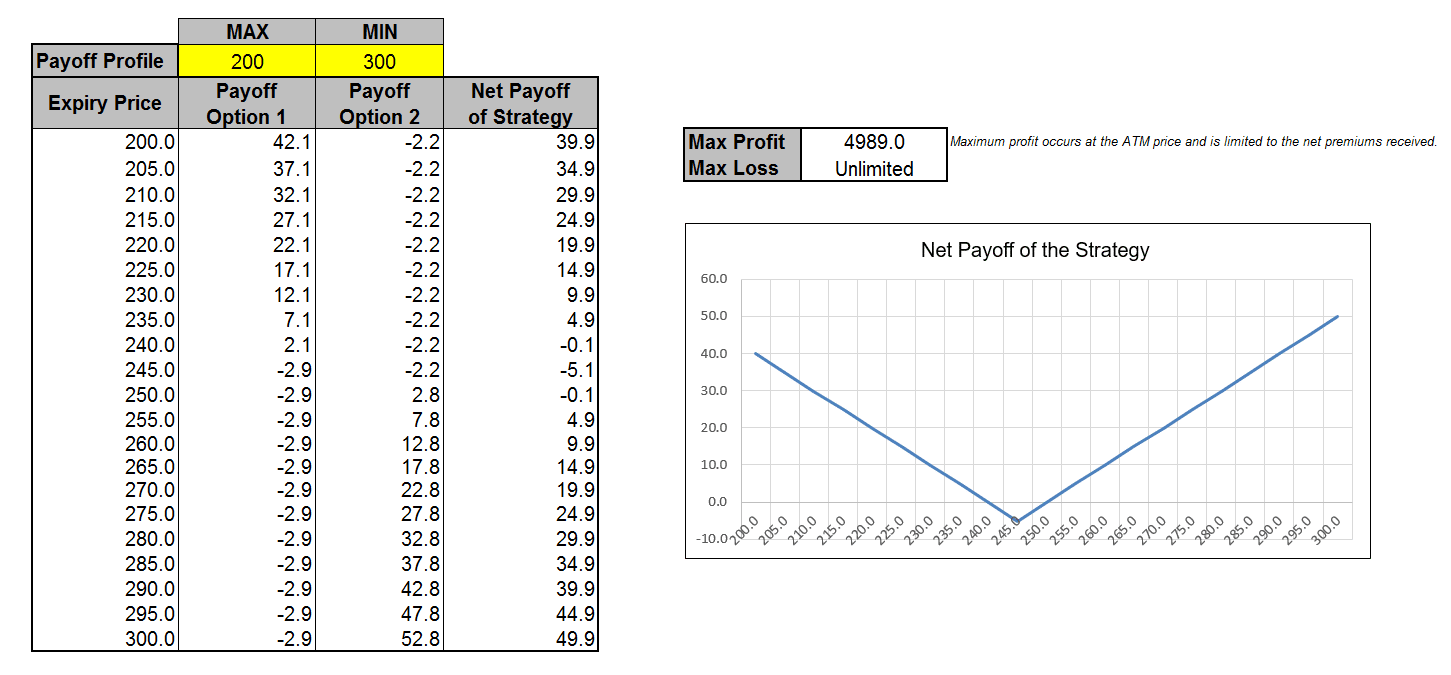

Max, min, breakeven

Normally traders calculate this manually based on various possible scenarios or the price of the underlying. The maximum profit is unlimited irrespective of the direction the underlying moves in. However, since a debit spread of $511 is created, the stock should move by around $5 on either side for a trader to at least break even on this trade. As I am writing this article, MSFT is trading at $245. Therefore, the breakeven point should be somewhere around $240 on the bearish side and $250 on the bullish side. Section 5 of the template shows the change in profit concerning the difference in the price of the underlying.

Key takeaways

1. The long straddle is a high volatility strategy. It is used when a trader expects the price movement to be maximum. The aim is to see that the stock moves sharply in one direction.

2. The long straddle is a beginner strategy as it doesn’t involve making further adjustments. Execute one call, and one put ATM trades simultaneously and leave it. As simple as that.

3. The profits are unlimited, provided the underlying goes berserk while the loss is limited to the premium paid to the writer.

4. A net debit spread is created to open a trade based on this strategy which means a certain amount is paid upfront in a premium.

Disclaimer

None of the content published on marketxls.com constitutes a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person.

The author is not offering any professional advice of any kind. The reader should consult a professional financial advisor to determine their suitability for any strategies discussed herein.

the article is written for helping users collect the required information from various sources deemed to be an authority in their content. The trademarks if any are the property of their owners and no representations are made.

References

Learn more about long straddle here.

Get Market data in Excel easy to use formulas

- Real-time Live Streaming Option Prices & Greeks in your Excel

- Historical (intraday) Options data in your Excel

- All US Stocks and Index options are included

- Real-time Option Order Flow

- Real-time prices and data on underlying stocks and indices

- Works on Windows, MAC or even online

- Implement MarketXLS formulas in your Excel sheets and make them come alive

- Save hours of time, streamline your option trading workflows

- Easy to use with formulas and pre-made templates

I invite you to book a demo with me or my team to save time, enhance your investment research, and streamline your workflows.