")

A leverage ratio is a financial measurement to check out what proportion of capital comes within in the kind of debt (loans) and assess the ability of a corporation to satisfy its financial obligations. The leverage ratio category is vital because companies rely on a mix of equity and debt to finance their operations, and knowing the quantity of debt held by a corporation is beneficial in evaluating whether it pays off its debts as they come due.

The financial leverage ratios measure the general debt load of a corporation and compare it with the assets or equity. This shows what proportion of the corporate assets belong to the shareholders instead of creditors. When shareholders own a majority of the assets, the corporate is claimed to be less leveraged. When creditors own a majority of the assets, the corporate is considered highly leveraged. All of those measurements are important for investors to know how risky the capital structure of a corporation is and if it’s worth investing in.

Leverage Types

1.) Operating leverage: Operating leverage is a formula that measures the degree to which a firm or project can increase operating income by increasing revenue. A business that generates sales with a higher gross margin and low variable costs has high operating leverage.

2.) Financial leverage: it is also called trading on equity. Financial leverage means the use of preference share capital, equity share capital along with fixed interest bearing securities or debentures i.e. debt. Financial leverage assumes that the firm is capable of earning more on assets than that acquired by use of funds, on which fixed rate of dividend/interest is paid.

3.) Combined leverage: This leverage shows the relationship between alteration in sales and the corresponding variation in taxable income. If the management feels that a certain percentage of change in sales would result in percentage change to taxable income they would like to know the level or degree of change.

How is Leverage Created?

• A corporation takes on debt to buy specific assets. This is referred to as “asset-backed lending” and is very common in real estate and purchases of fixed assets like property, plant, and equipment (PP&E).

Common leverage ratios

There are several different leverage ratios that may be considered by market analysts, investors, or lenders. Some accounts that are considered to have significant comparability to debt are total assets, total equity, operating expenses, and incomes.

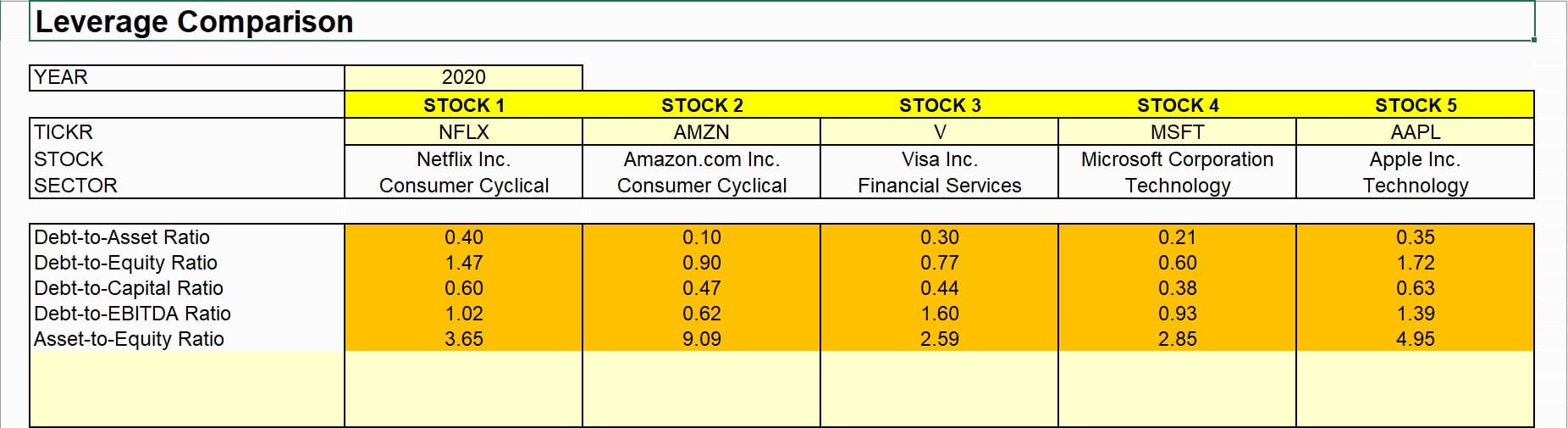

Debt-to-Assets Ratio = Total Debt / Total Assets

Debt-to-Equity Ratio = Total Debt / Total Equity

In short, Debt Equity ratio helps us see the proportion of debt and equity in the capital structure of the company. For example, if a company is too dependent on debt, then the company is too risky to invest in. On the other hand, if a company doesn’t take debt at all, it may lose out on the benefits of leverage.

Debt-to-Capital Ratio = Today Debt / (Total Debt + Total Equity)

The debt-to-capital ratio gives analysts and investors an enhanced idea of a company’s financial structure and whether or not the company is a suitable investment. All else being equal, the higher the debt-to-capital ratio, the riskier the company. This is because a higher ratio, the more the company is financed by debt than equity, which means a higher liability to repay the interest and principal payments and a greater risk of defaulting on the loan if the debt cannot be paid timely.

Debt-to-EBITDA Ratio = Total Debt / Earnings Before Interest Taxes Depreciation & Amortization (EBITDA)

This leverage ratio is the ultimate ratio that finds out how much impact debt has on the revenues of a company. And since a company needs to pay interests (cost of debt), this ratio will have a huge impact on the company’s revenues. For example, if the debt is more, the interests would be more (possibly, if the cost of debt is higher) and as a result, the taxes would be less and vice versa.

Asset-to-Equity Ratio = Total Assets / Total Equity

There is no standard Asset to Equity ratio but it is valuable in comparing to similar businesses and industries. A relatively high ratio (indicating more of assets and very little equity) may indicate the company has taken on substantial debt merely to remain in business but a high Asset to Equity ratio can also mean the return on borrowed capital exceeds the cost of that capital.

At some higher levels, however, the ratio can reach unsustainable levels, as the additional debt intensifies up interest costs and the deteriorating financial position puts the firm in difficulty.

How to Find Important Leverage Ratios Using MarketXLS Template?

Step 1: Enter year in the cell C3. Then Enter up to 5 stocks (Ticker symbols) to be compared in the cell range (C5:G5). Here I have taken the stocks of Netflix, Amazon, Visa, Microsoft and Apple each from consumer cyclical, financial and technology sectors for the year 2020. You can also compare stocks from the same sectors to get their respective leverage ratios.

Step 2: As soon as you press enter, stocks’ names and sectors will appear. Further, the calculated important leverage ratios can be seen below it.

Link to this Template: https://marketxls.com/template/leverages-analysis-low-debt-companies-ratio-analysis/

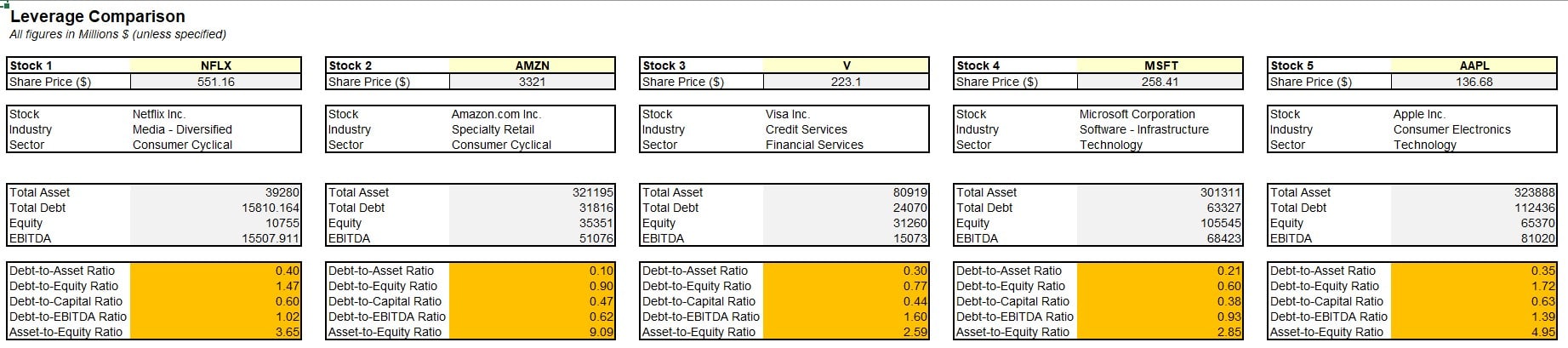

Step 3: To further understand the calculation of leverage ratios, please switch to the CALCULATION sheet. The calculation sheet contains all the related data and information about the company’s earnings, total assets, debt and equity structure. It will appear like this:

With the help of MarketXLS, you can stream market data for stocks, ETFs, options, mutual funds, currencies refreshed, or refresh on-demand. You can also get all the historical data (EOD, Intraday) you may need with MarketXLS functions in a few clicks. Update the Excel tables dynamically and save your time in formatting those tables. Also get access to variety of templates like this and compare your portfolio stocks to get better analysis of your investments.

Risks of High Operating Leverage and High Financial Leverage

If leverage can increase earnings, it can also increase risk. Having both high operating and financial leverage ratios can be quite problematic for a business. A high operating leverage ratio explains that a company is generating few sales, still has high costs or margins that need to be covered. This may either result in a lower profit target or insufficient operating income to cover other expenses and will result in negative earnings for the company. On the other hand, high financial leverage ratios occur when the return on investment (ROI) does not surpass the interest paid on loans. This will significantly decrease the company’s profitability and earnings per share.

Bottom Line

As investors, you need to look at everything. Leverage ratios will help you how a company has structured its capital. Many companies don’t like to take loans from outside. They believe that they should fund all their expansion or new projects through equity.

But to take advantage of leverage, it’s important to structure the capital with a proprotion of the debt. It helps reduce the cost of capital (by reducing the cost of equity, it is huge). Plus, it also helps in paying less tax since the interest payments are tax deductible (i.e. the cost of debt).

If the company has taken too much debt, it’s too risky to invest in the company. At the same time, if a company doesn’t have any debt, it may pay off too much in cost of capital and actually reduce their earnings in the long run.

But only leverage ratios won’t help. You need to look at all the financial statements (especially four – cash flow statement, income statement, balance sheet, and shareholders’ equity statement) and all other ratios to get a concrete idea about how a company is doing. However, it surely does help investors in deciding whether a company is taking advantage of the leverage or not.

Disclaimer

Reference

For related articles, click here.