Using Vwap Strategy For Option Trading

Meet The Ultimate Excel Solution for Investors

- Live Streaming Prices Prices in your Excel

- All historical (intraday) data in your Excel

- Real time option greeks and analytics in your Excel

- Leading data in Excel service for Investment Managers, RIAs, Asset Managers, Financial Analysts, and Individual Investors.

- Easy to use with formulas and pre-made sheets

Stock charts are good for telling the story of a price over a given time period. But they can also create a lot of noise and potentially make it hard to identify the most important prices. That’s why people use VWAP, or volume weighted average price, to find the price at which all the action took place.

Volume weighted average price (VWAP) and moving volume weighted average price (moving VWAP, or sometimes MVWAP) are a type of weighted average and works on the principle of averaging the traded price in terms of volume traded.

Most traders use VWAP Strategy for intraday trading. Price below VWAP may indicate that security is ‘cheap’ and, a price above VWAP indicates that security is ‘expensive’ on an intraday basis.

Understanding VWAP

Let us assume a stock opens at the low of the day at $80 and then closes at $110. A candlestick for that day will show a black or green candle spanning from $80 to $110.

However, that doesn’t give us the complete picture. Let’s say that there were a lot of trades that happened at the $90 level. While the trading technically ranged from $80 to $110 that day, the majority of the trade occurred at $90. The VWAP will be representative of that and show $90 as the best representation of the stock’s true price for that given day.

Calculation

VWAP is calculated automatically in one’s charting software. However, for our better understanding let us look at the calculation.

VWAP is calculated using the below steps-

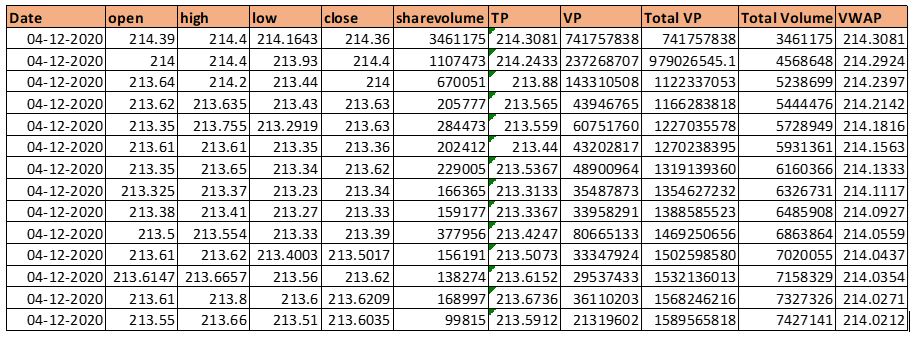

1. Typical price = which is the average price of High, Low, and close

2. Volume Price (VP) = we get this by multiplying the typical price with its volume

3. Total VP = This is a cumulative number, which is the sum of the current VP and the previous VP

4. Total volume = This is again a cumulative number, which is the sum of the current volume and the previous volume

5. VWAP = We get this VWAP number by dividing the Total VP by Total Volume. The resulting number indicates the average traded price, weighted by volume.

Moving VWAP is simply adding up various end-of-day VWAP figures and averaging them out over a user-specified number of periods.

Example

Let’s calculate VWAP for Microsoft stock for 4 December 2020–

As you can see, the VWAP is a dynamic number, changing based on how the trades flow in.

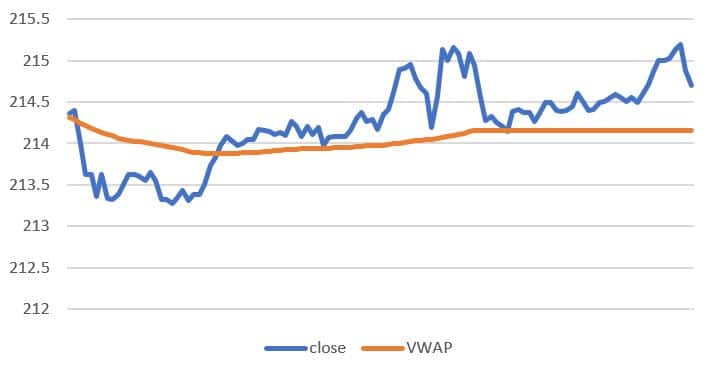

Candlestick chart for 4/12/2020

I have plotted the closing price along with VWAP for better understanding.

How to use the VWAP?

1. As already said VWAP is an intraday indicator, hence, it is best used on a 5 or 10-minute chart. Often when you plot this, you will notice a jump at the start of the day, when compared to the previous day’s data.

2. VWAP is an average and like any indicators employing averages, this too lags the current market price

3. VWAP is used for 2 main reasons – to get a sense of intraday direction and to get a sense of the efficiency of order execution

4. If the current price is below VWAP, then the general opinion is that the intraday trend is down

5. If the current price is above VWAP, then the general opinion is that the stock is trending higher

6. If the VWAP lies in between the high and low, then the expectation is that the stock will remain volatile

7. If you intend to short a stock, then it is considered an efficient fill if you short the stock at a price higher than VWAP

8. Likewise, if you intend to go long on a stock, then it is considered an efficient fill if you go long at a price lower than VWAP

VWAP for effective trading

• Traders use VWAP for a number of different strategies. One simple day-trading strategy is to buy when a stock’s price crosses above a stock’s 5-minute VWAP, using the previous period’s VWAP as a stop. This type of crossover can be an indication that buyers are stepping in.

• Some traders simply use VWAP to time their short-term entry and exit points. When a stock is trading above its VWAP, it’s generally seen as a good relative price at which to sell. This strategy assumes that a stock’s “true” price is its VWAP.

• Traders also use a mean-reversion type trading strategy centered on VWAP. This mean-reversion strategy assumes that a stock’s share price will generally tend to come back to its VWAP over time. When a stock’s share price gets too far above its VWAP, mean-reversion traders sell. When the share price gets too far below, they buy.

Disclaimer

None of the content published on marketxls.com constitutes a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The author is not offering any professional advice of any kind. The reader should consult a professional financial advisor to determine their suitability for any strategies discussed herein.

References

https://www.daytrading.com/vwap

https://tradingsim.com/blog/vwap-indicator/

https://www.lightspeed.com/active-trading-blog/what-is-vwap

Get Market data in Excel easy to use formulas

- Real-time Live Streaming Option Prices & Greeks in your Excel

- Historical (intraday) Options data in your Excel

- All US Stocks and Index options are included

- Real-time Option Order Flow

- Real-time prices and data on underlying stocks and indices

- Works on Windows, MAC or even online

- Implement MarketXLS formulas in your Excel sheets and make them come alive

- Save hours of time, streamline your option trading workflows

- Easy to use with formulas and pre-made templates

I invite you to book a demo with me or my team to save time, enhance your investment research, and streamline your workflows.