Long Call Diagonal Spread – An Advance Option Strategy

Meet The Ultimate Excel Solution for Investors

- Live Streaming Prices Prices in your Excel

- All historical (intraday) data in your Excel

- Real time option greeks and analytics in your Excel

- Leading data in Excel service for Investment Managers, RIAs, Asset Managers, Financial Analysts, and Individual Investors.

- Easy to use with formulas and pre-made sheets

What is a Diagonal Spread?

A Diagonal Spread is the options strategy that combines horizontal spread (calendar spread) and vertical spread. It involves simultaneously buying and selling of the same class of options with different strikes and expiration dates. The term “diagonal” comes from the options chain layout where the two options contract with different strikes price and expiration dates would be diagonally oriented.

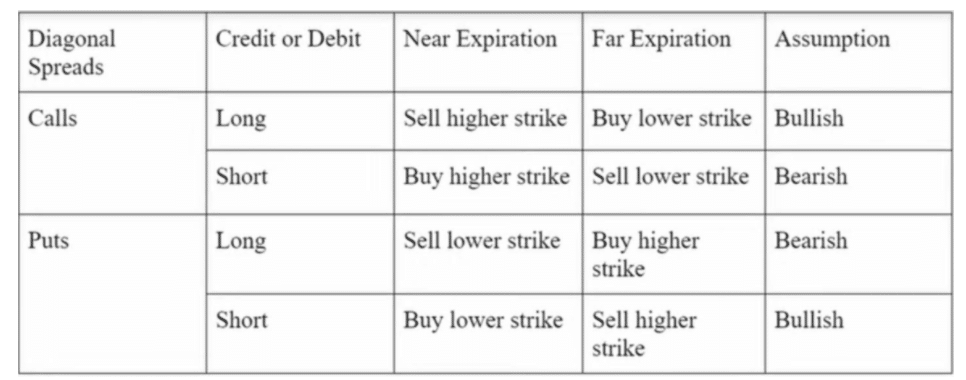

How to built up Diagonal Spread?

We can build a diagonal spread by using two call options or two put options. One should be of near month expiration, and another one should of far month expiration. Also, one option’s strike price must be higher, and the strike price of another one must be lower. It depends upon your view of how you want to build the diagonal spread.

Long Call Diagonal Spread

Long call diagonal spread is implemented by buying a call option of a lower strike price expiring in the far month and selling a call option of a higher strike price expiring in the near month. It is also called Poor’s man covered call because we can buy a call option instead of owning 100 stocks and can sell a call against it with a low capital requirement. This strategy gives a benefit of vertical and calendar spread in terms of long delta and time decay.

View – Bullish

Setup

XYZ stock is currently trading at $50.

Long 1 ITM Mar 45 call option at $15

Short 1 OTM Feb 55 call option at $5

Net Debit= $10.

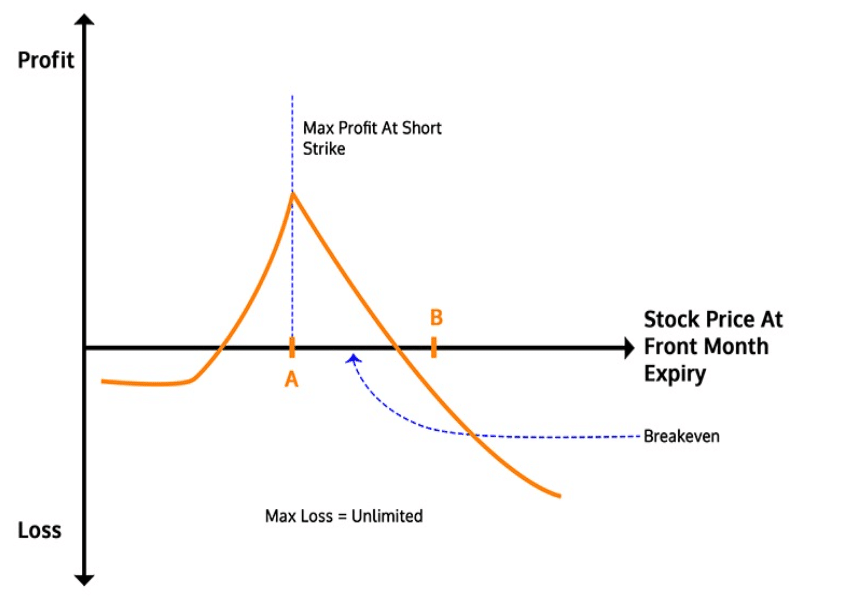

Maximum Profit

The maximum profit is realized if the stock price is equal to the short call’s strike price on the short call’s expiration date. We cannot figure out the exact maximum profit since it depends on the long call price and its implied volatility. However, the potential payoff is calculated with the following formula:

Width of the call strikes – Net Premium paid

Maximum Risk

- If established for the net credit-

Maximum Risk = Difference between strike prices – Net Credit Received. - If established for the net debit-

Maximum Risk = Difference between strike prices + Net Premium paid.

Long Diagonal Call Spread vs. Long Calendar Call Spread vs. Long Vertical Call Spread

Currently, Microsoft(MSFT) is at $239.50 (05 Feb, 21). We have built long call diagonal spread, Long Calendar spread, and long vertical spread using different strike prices and expiration dates.

- Long Delta

In-the-Money (ITM) options have a higher delta than the Out-of-the-Money options (OTM). Delta of the long options is positive, while that of the short options is negative. By longing for ITM call options, we are buying a positive delta, which will increase the net delta of the strategy. A Higher Positive delta will increase the higher premium if the stock moves in an upward direction. - Time Decay (Theta)

Time decay accelerates when the options approach the expiration date.

Therefore, Theta has more impact on the front month short option than the back month-long option. Theta of the near-term option is higher than the far month option. Since we have short, the near-term option decay happens faster, and at the expiration, the option loses its value and becomes worthless. While the long option decays at a slower rate as compared to the near-term short option. - High Vega

Volatility tends to show a greater boost in the value of the back month option we are long, compared to the negative impacts of the front-month option we are short. Since Vega is higher for the far-term options and lower for the near-term options, we are buying higher Vega and selling lower Vega. An increase in the implied volatility in the back month option creates a favorable impact on this strategy, everything else being equal.

Short Call Diagonal Spread

In the case of a bearish view, one can build a short call diagonal spread.

In the short call diagonal spread, we sell the longer-term option having the lower strike price and buy the near-term option with a higher strike price—generally, this strategy builds on net credit. This strategy involves limited risk and limited profit potential.

Setup

Buy Feb 55 call option at $10

Sell Mar 45 Call option at $15

Net credit received = $5

Maximum Profit

The maximum profit is equal to the net credit received (commissions excluded). If the stock price falls below the short call, then the short call expires worthless, and the entire premium will be treated as profit.

Maximum Risk

The maximum risk is realized if the stock price is equal to the long call’s strike price on the long call’s expiration date. The loss equals the price of the short call minus the net credit received.

Conclusion

The Diagonal call spread is an advanced strategy, so one must continuously observe the stock’s position. We have to take care of various other factors like time decay, volatility, delta, gamma, price of the underlying asset, etc. One must appropriately select the strike prices and expiration dates. It is advisable to roll over the position if the direction or the option greeks goes against you.

Disclaimer

None of the content published on marketxls.com constitutes a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The author is not offering any professional advice of any kind. The reader should consult a professional financial advisor to determine their suitability for any strategies discussed herein.

Reference

To know more about option greeks, click here.

To know more about the diagonal spread, click here.

Get Market data in Excel easy to use formulas

- Real-time Live Streaming Option Prices & Greeks in your Excel

- Historical (intraday) Options data in your Excel

- All US Stocks and Index options are included

- Real-time Option Order Flow

- Real-time prices and data on underlying stocks and indices

- Works on Windows, MAC or even online

- Implement MarketXLS formulas in your Excel sheets and make them come alive

- Save hours of time, streamline your option trading workflows

- Easy to use with formulas and pre-made templates

I invite you to book a demo with me or my team to save time, enhance your investment research, and streamline your workflows.